|

|

|

|

FEI

Cash Bids

Market Data

News

Ag Commentary

Weather

Resources

|

Can Nvidia Keep Its AI Crown?/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

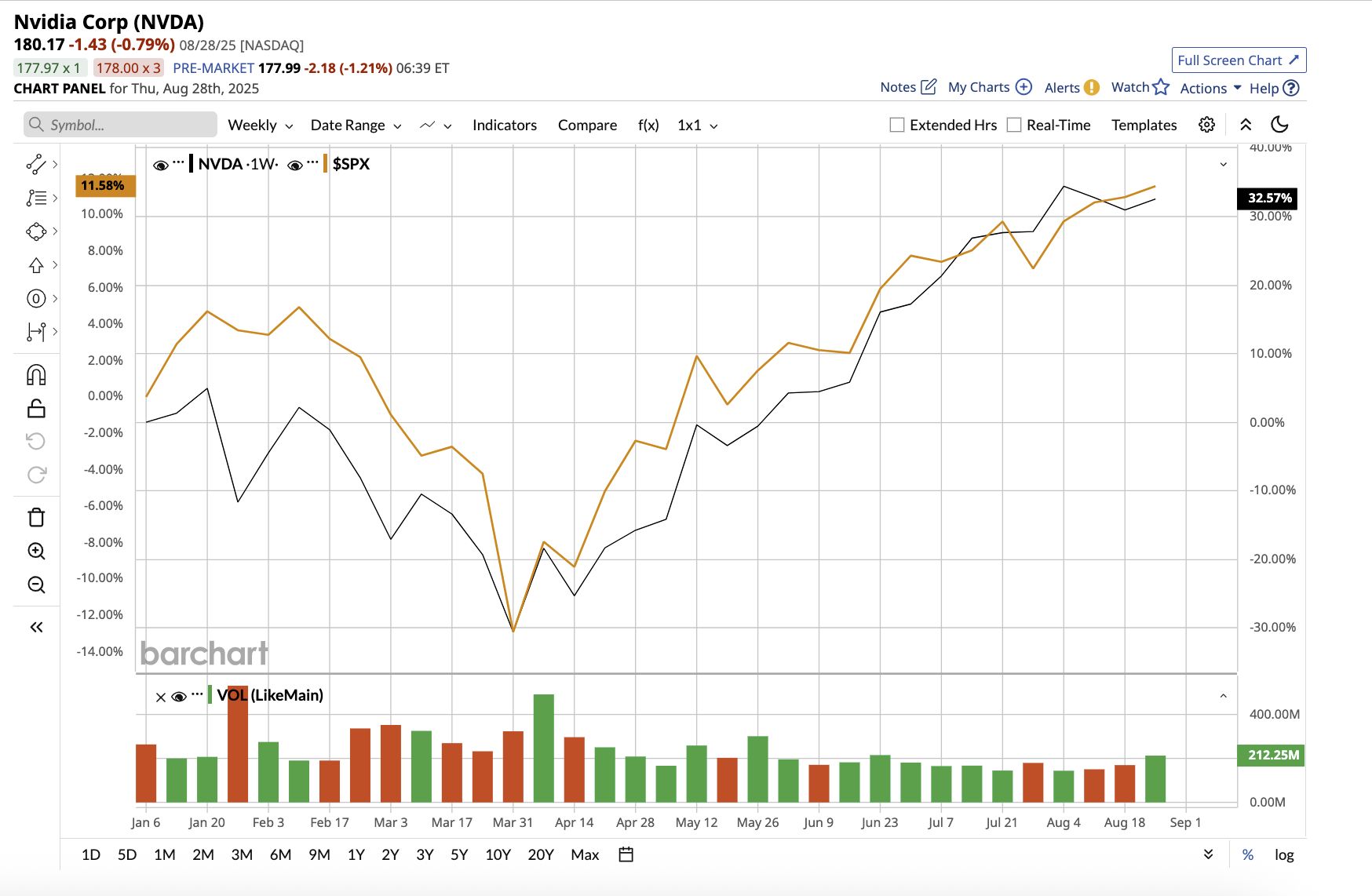

Valued at $4.4 trillion, Nvidia (NVDA) continues to prove why it holds the title as the most important company in the artificial intelligence (AI) ecosystem. The company reported another strong quarter in computing, networking, gaming, robotics, and automotive, demonstrating that its leadership extends well beyond graphic processing units (GPUs). So far this year, the stock is up 30%, outperforming the broader market. Let’s find out if Nvidia can maintain its AI dominance as competition heats up and geopolitical risks grow.

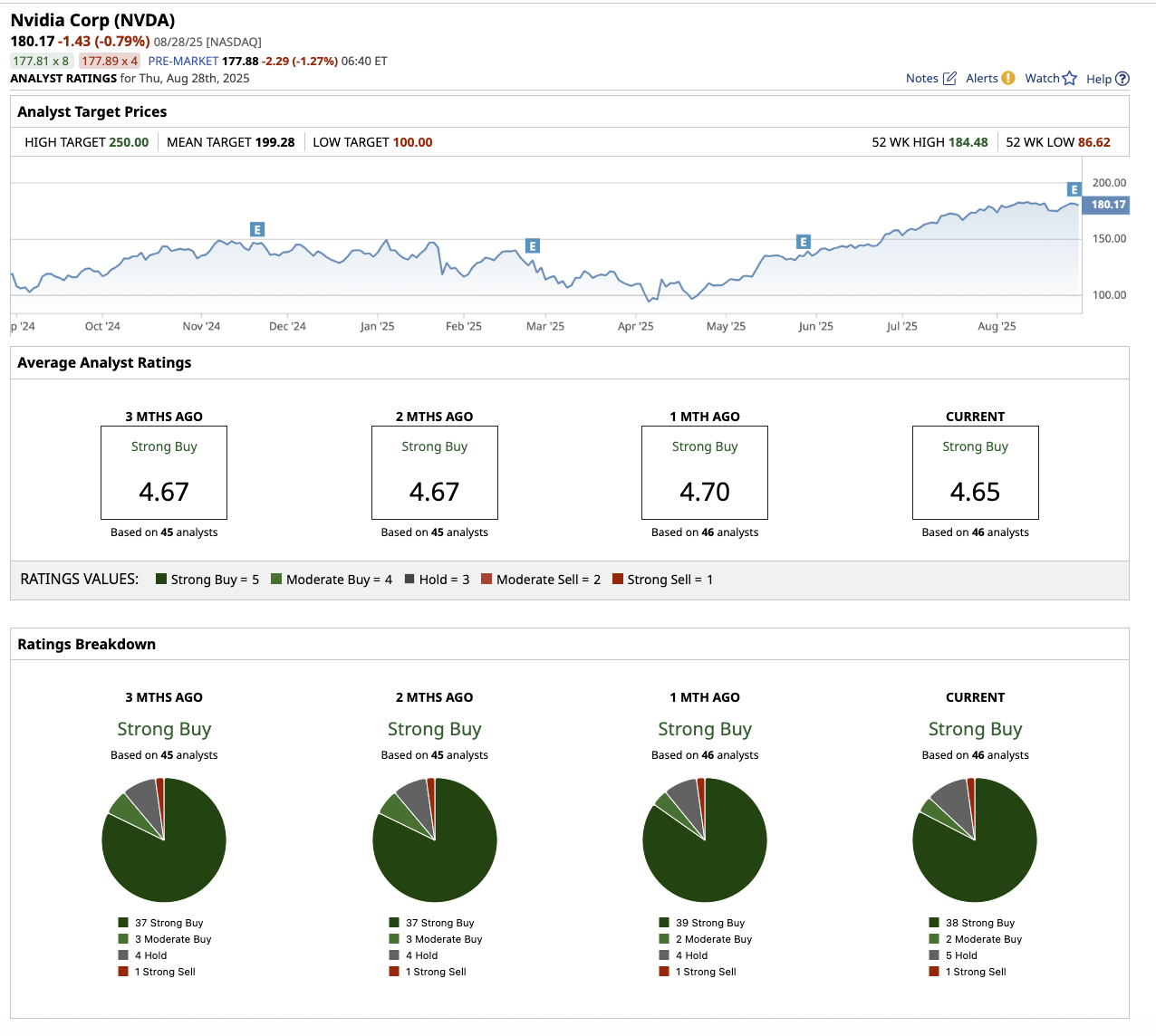

Nvidia Did It Again With a Robust Q2Nvidia’s second-quarter fiscal 2026 results proved once again that it is the most powerful force in the AI ecosystem. It reported $46.7 billion in revenue, exceeding expectations and continuing its streak of historic growth. Data center revenue, now the company’s growth engine, increased 56% year over year. Nvidia’s latest GPU generation, the Blackwell platform, is already setting a new standard for AI training and inference. Nvidia’s gaming business also reached new heights, generating $4.3 billion in revenue, a 49% increase. Growth was driven by the increased production of Blackwell GeForce GPUs, which are still in short supply due to high demand. Professional visualization revenue increased 32% to $601 million, owing to strong demand for AI-accelerated design, simulation, and prototyping. Automotive revenue increased by 69% year over year to $586 million, fueled by Nvidia's push into self-driving compute. While Nvidia is well-known for its hardware, it is its software stack that keeps customers coming back. The CUDA ecosystem has developed a formidable moat. Millions of developers worldwide are creating workflows on it. Beyond networking, Nvidia is expanding its presence in areas that could become the next multibillion-dollar market. Its CUDA-Q quantum platform now works with over 300 ecosystem partners, including AWS, Quantinuum, and Google (GOOGL) Quantum AI. Meanwhile, the company introduced Nvidia Thor, a new robotics computing platform with 10 times the AI performance and efficiency of its predecessor, Orin. Leading companies such as Amazon Robotics, Boston Dynamics, Caterpillar (CAT), Figure AI, Medtronic (MDT), and Meta (META) are using Thor to enable cutting-edge robotic applications. The company is ensuring that robotics will be a long-term demand driver for Nvidia’s data center business. Geopolitical Tensions Exist, But Demand Outpaces SupplyDespite the impressive product roadmap, not everything is in Nvidia’s control. In late July, the U.S. government began reviewing licenses for selling the H20 chip to Chinese consumers. If geopolitical tensions ease, the company expects to ship $2 billion to $5 billion in H20 revenue in the third quarter alone. The stakes are high, with China being one of the largest markets for AI infrastructure. Management believes that prolonged restrictions will allow domestic Chinese competitors to grow. Even with these headwinds, Nvidia is struggling to keep up with rising demand. Nvidia predicts that $3 trillion to $4 trillion will be spent on AI infrastructure by the end of the decade, including sovereign AI projects, enterprise adoption, and the rise of physical AI in robotics. The company is positioning itself as the default provider of this infrastructure, not just through GPUs, but through its entire ecosystem. Nvidia’s financial position remains as strong as its technological pipeline. The company reported adjusted gross margins of 72.7%, with a modest boost from an H20 inventory release. Inventory increased from $11 billion to $15 billion in the second quarter to support Blackwell and Blackwell Ultra. Nonetheless, the company maintains discipline in capital allocation, returning $10 billion to shareholders in the quarter through buybacks and dividends. Furthermore, the board approved an additional $60 billion share repurchase program. Nvidia ended the quarter with $56.8 billion in cash, cash equivalents, and marketable securities. Looking ahead, Nvidia expects $54 billion in revenue in Q3, plus or minus 2%, with gross margins rising to around 73%. Importantly, management emphasized that this outlook excludes any H20 shipments to China, allowing for potential upside if geopolitical conditions improve. Analysts who follow the stock predict a 58% increase in revenue to $206.1 billion in fiscal 2026, followed by a 49.8% increase in earnings. Revenue and earnings could increase by 31.1% and 40.5%, respectively, in fiscal 2027. Currently, Nvidia stock is trading at 40 times forward earnings. Is Nvidia Stock a Buy, Hold, or Sell on Wall Street?Overall, Nvidia stock is a “Strong Buy” on Wall Street. Out of the 46 analysts that cover the stock, 38 have a “Strong Buy” recommendation, with two “Moderate Buy” ratings, five “Hold” ratings and one “Strong Sell” rating. The average target price for Nvidia stock is $199.28, which implies potential upside of 10.6% over the next 12 months. The high price estimate of $250 implies the stock can rally as much as 39% from current levels.

Can Nvidia Keep Its AI Crown?As AI spending approaches trillions of dollars, Nvidia’s position at the heart of the AI ecosystem appears as secure as ever. For now, it appears that Nvidia will maintain its AI leadership. Investors must watch to see if Nvidia can continue to balance explosive demand with supply constraints while dealing with competition and headwinds aimed at diminishing its dominant position. On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here. |

|

|