|

|

|

|

FEI

Cash Bids

Market Data

News

Ag Commentary

Weather

Resources

|

Grains finally catch a bullish bid into Labor Day weekend

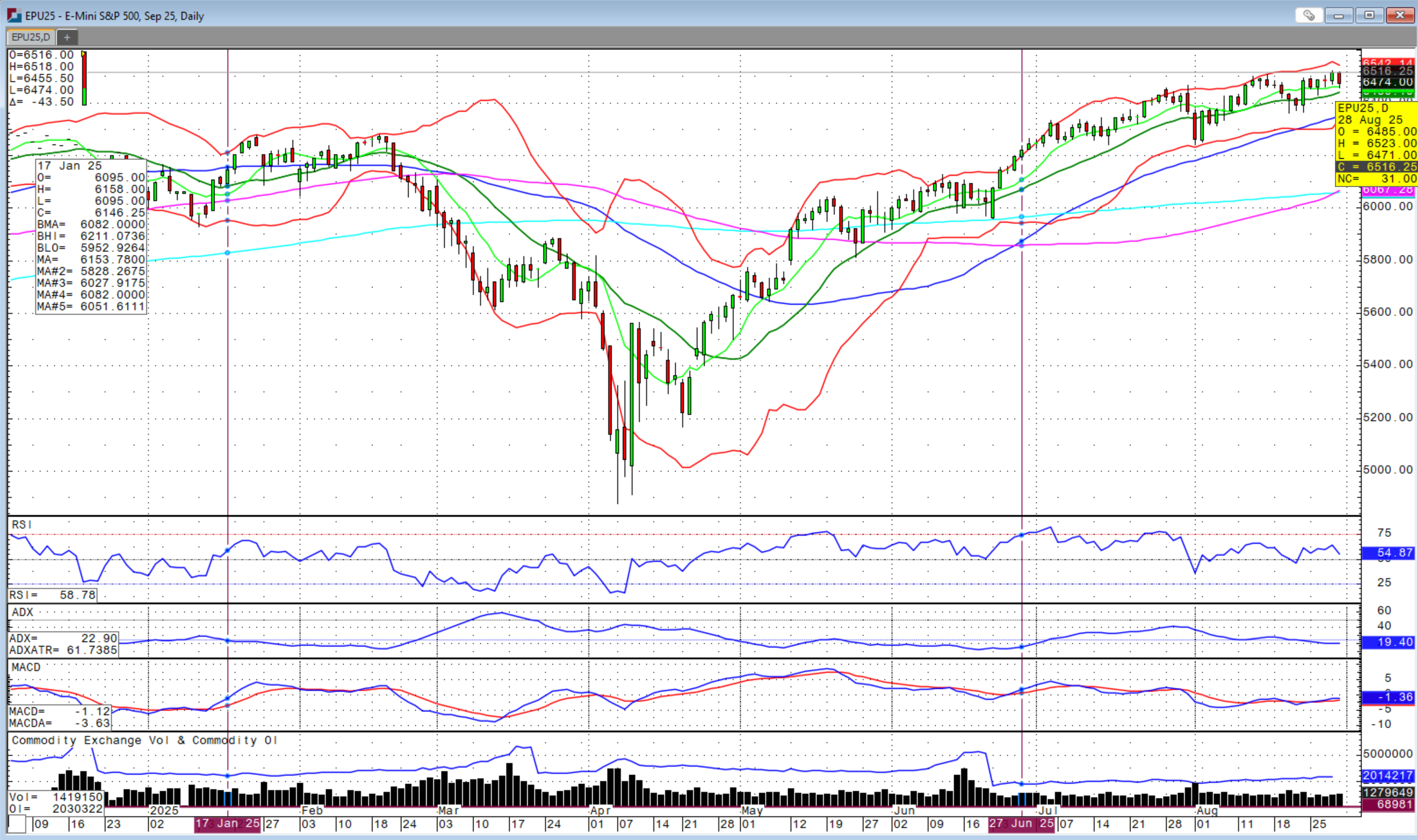

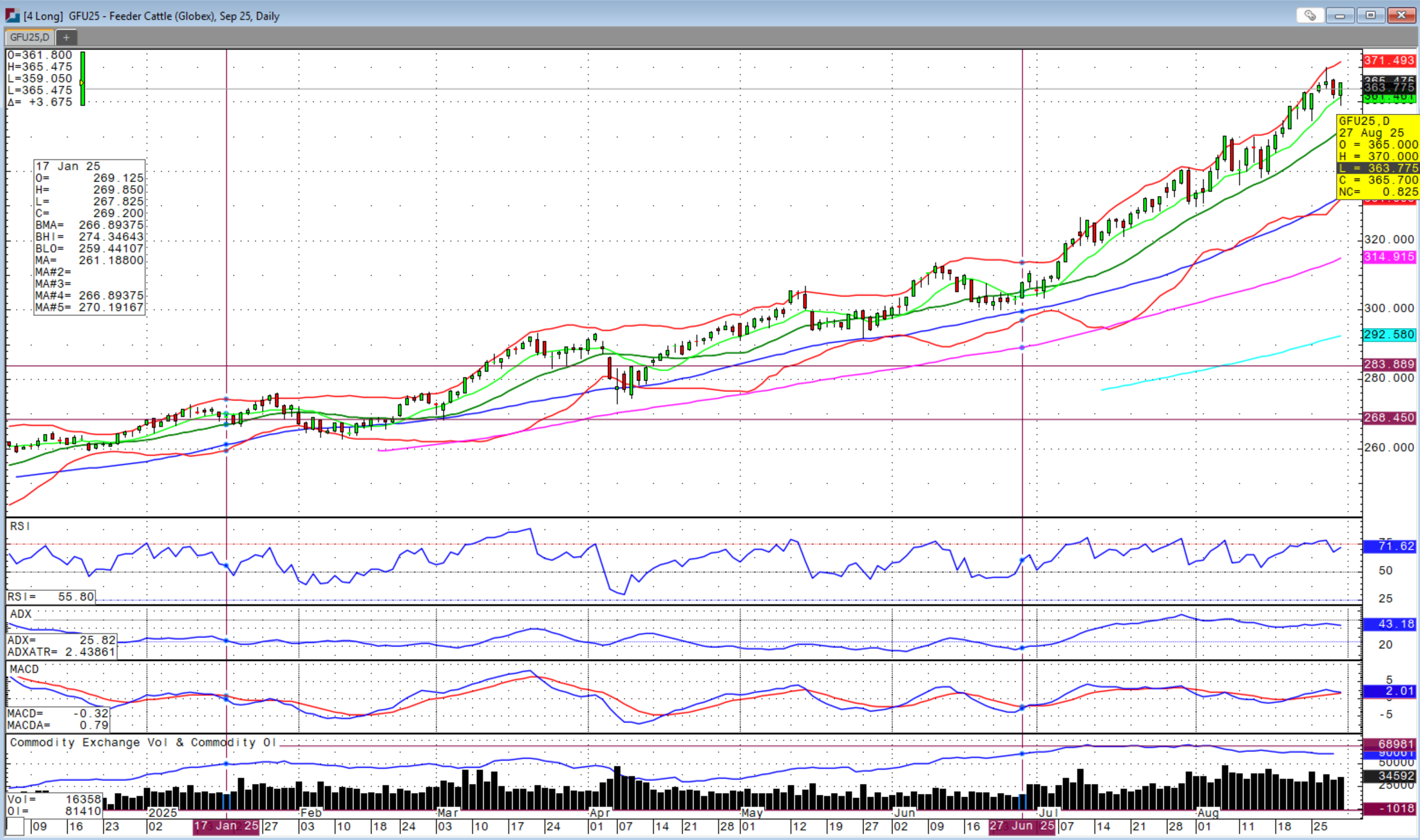

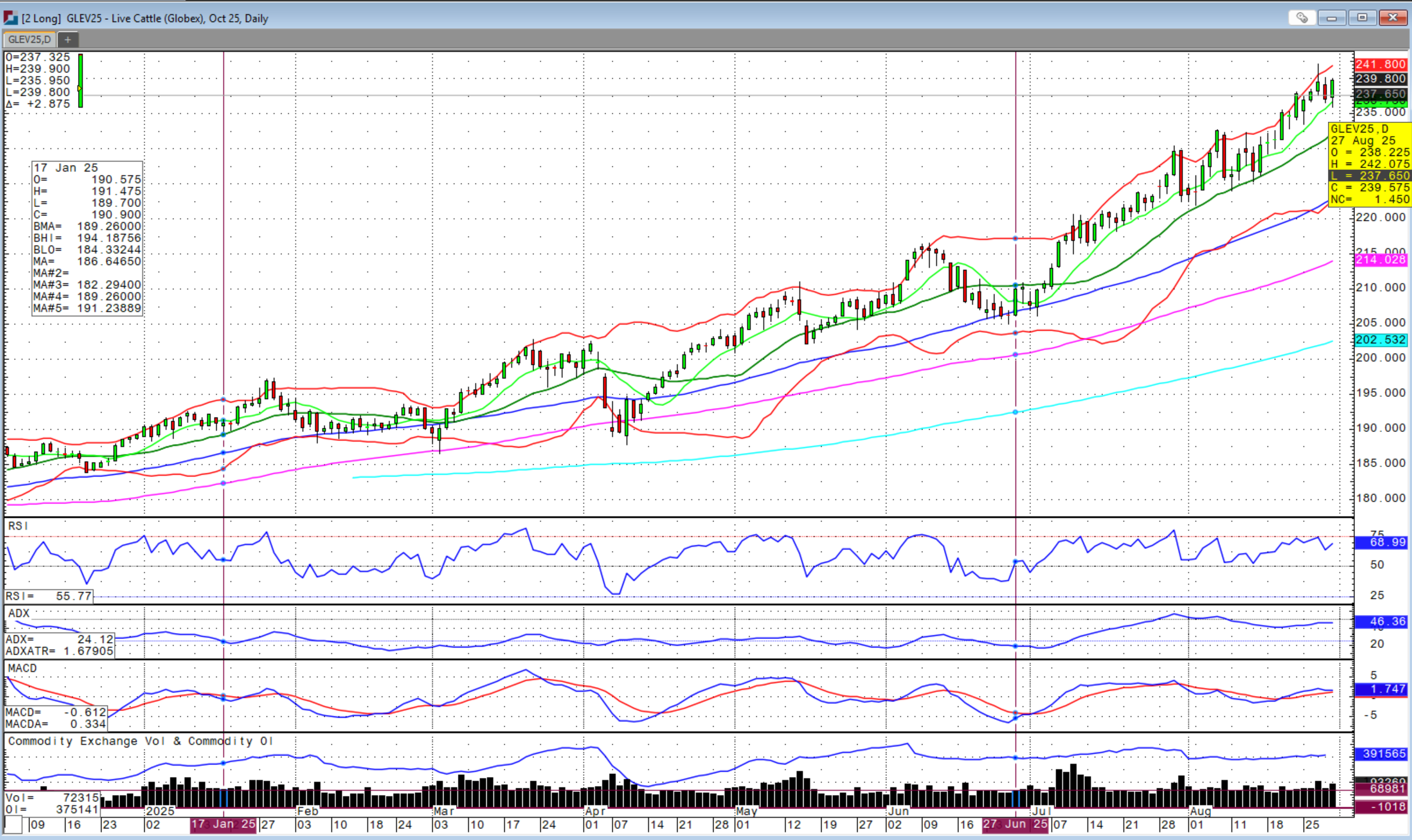

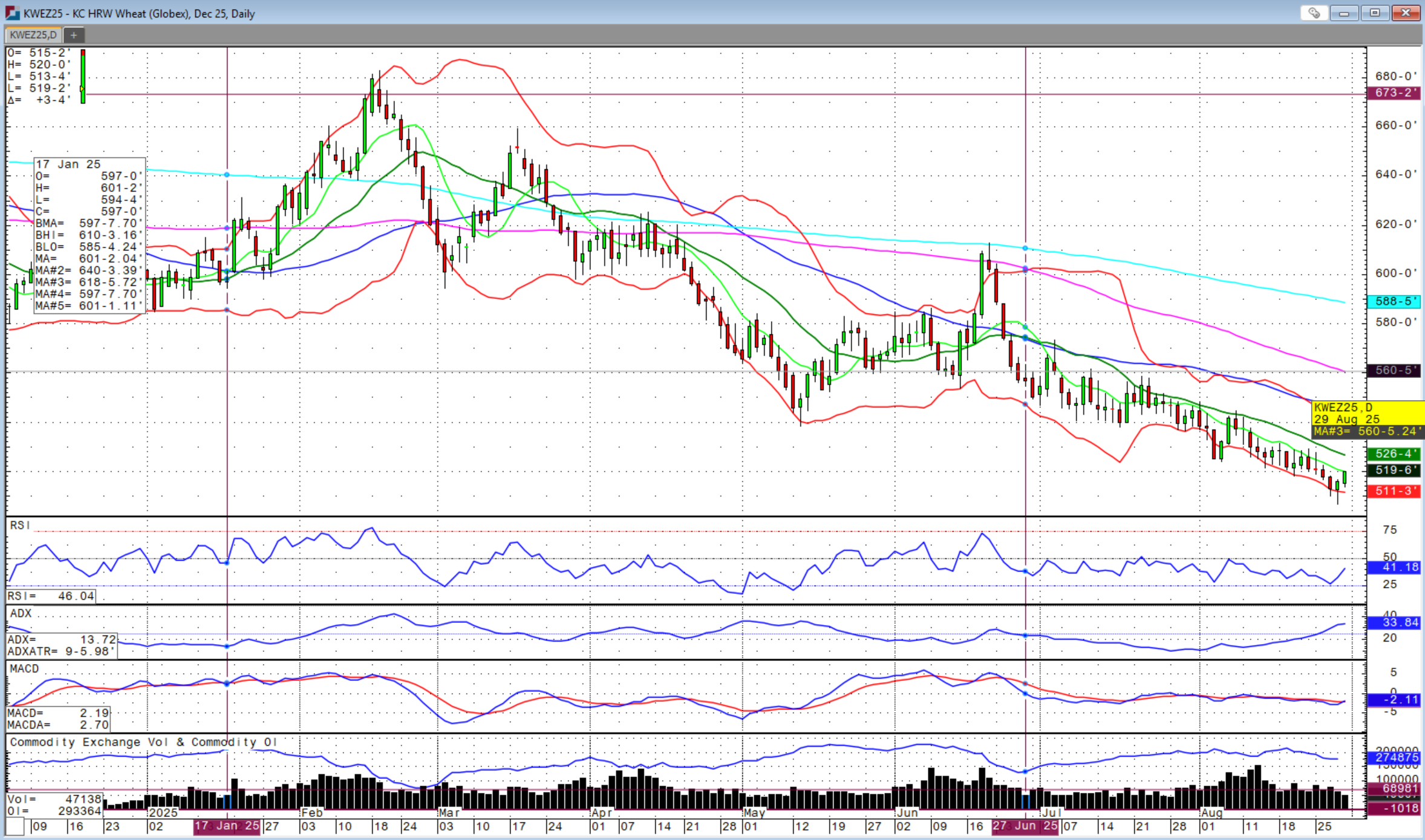

Happy Labor Day weekend market watchers!  Consumers all around are in tight positions and many are struggling, but the data keeps pointing to strength, making the case against interest rate cuts. When will these two stories converge and which side is closer to the true situation? It seems that some post-Labor Day weekend squeeze could emerge as the officially unofficial end to summer is here. The holidays are approaching and that will be the real test of consumer strength. The tariffs have created conundrums for retailers and added cost. Will consumers see higher costs during the holidays, and will they be able to afford it? Watch the jobs data these next couple months as that is beginning to show signs of softness that could be the real catalyst to stall this consumer. However, until then, the cattle markets continue to run wild, literally.  Cash fed cattle were the highlight to close the week with a new record $242 traded in Texas and $245 traded again in Nebraska. The spread between southern and northern bids has drastically narrowed and could indicate some topping action in the willingness of packers to pay more. But do they have a choice? That’s what the feedlots deny as they continue to be in the driver’s seat. Know that plenty of games are being played among the packers to try and outlast the weaker packers in this environment of negative margins. The cattle market has been crazy, but as they say, markets can be irrational longer than ‘you’ can stay liquid. If you’re staying short, risk manage with call options as I don’t think we’re done yet based on Friday’s move. However, absolutely anything can happen in this market environment without forewarning.  The grain markets are finally showing signs of life worth talking about. Thursday’s outside reversal higher day followed by Friday’s breakout higher above the 50-day moving average showed some encouraging signs. The above chart gap from July 3rd is at $4.32 ¾, just above the 100-day moving average. While more talk of disease issues and flash droughts are emerging in parts of the corn belt, expect there to be a lot of farmer selling on any significant rallies especially with weak basis levels.  The other factor playing into this is the falling basis in soybean cash bids given the lack of China business. This may lead to farmers needing to store soybeans versus corn and therefore selling more cash corn now through harvest in addition to the large crop in the field. US corn conditions held steady at 71 percent Good-to-Excellent (G/E), one percent ahead of expectations, and remains the best in 9 years. US soybean conditions improved one percent from last week, but two percent above expectations, now also the best in 9 years for late August.  Seasonally, we typically find some strength this time of year after a post-harvest selloff. This week last year was the bottom followed by a near $1.00 rally into the end of September. Let’s hope there is some continued strength ahead in the grain markets after the recent weakness well below breakeven levels for producers. If you need to sell grain at these levels, take a small portion of the cash grain check and re-own those bushels on the Board. Option volatility is low as are prices and so call options are very reasonable as is the time value to go out to March contracts.  If you need to sell to pay bills, that doesn’t mean you have to be out of the market and watch it rally. You can stay in the game without owning the physical bushels and having to pay storage. Just buy the call option for a fraction of what it cost to own the physical bushels and stay in the game. Yes, there is terminology involved, but that’s why Sidwell Strategies is here. Just give us a call and we will advise and execute on how to achieve your cash flow needs and profit margin goals. Reach out and use the tools that are there for you instead of blindly holding grain and paying elevator storage until you absolutely have to sell it. Once you see the numbers and ability to do more with less, you will not be able to unsee it. US spring wheat conditions declined this week in the final condition rating of the year and could add some underlying support to this market. Ultimately, we need the managed funds to cover shorts and be buyers in the grain complex, which I believe is about to take place at least to some degree.

This article contains syndicated content. We have not reviewed, approved, or endorsed the content, and may receive compensation for placement of the content on this site. For more information please view the Barchart Disclosure Policy here.

|

|

|